Pentair Stock Plunges After Slashing 2026 Outlook as Pool Inventory Destocking Weighs on Results

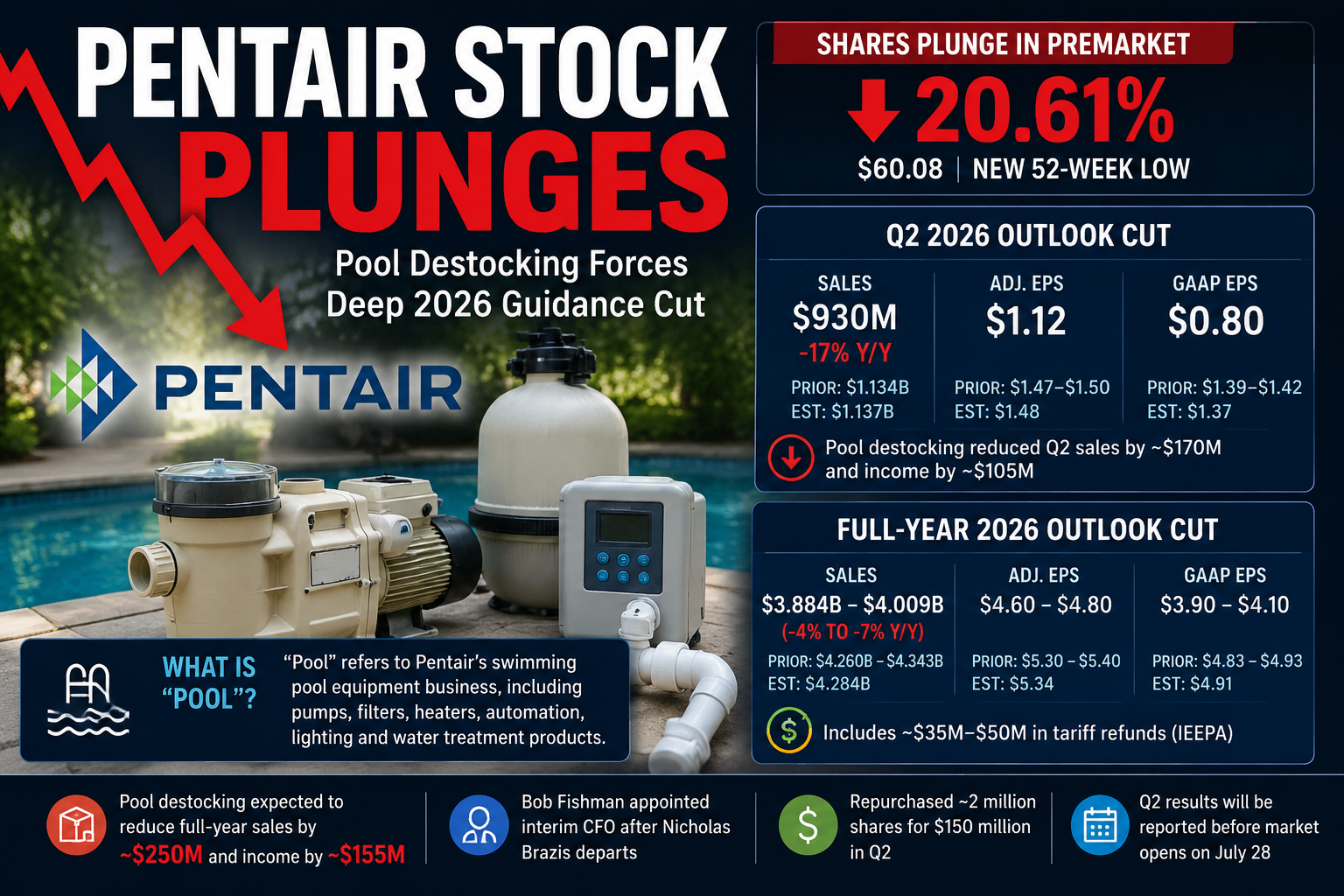

Pentair stock plunges more than 20% in premarket trading after the water treatment and pool equipment manufacturer dramatically cut its second-quarter and full-year 2026 guidance. The company blamed an unexpectedly severe reduction in inventory among swimming pool distributors and retailers, triggering one of its largest guidance resets in years.

The sharp decline sent shares to a new 52-week low as investors reacted to weaker sales expectations, lower earnings forecasts, and management’s warning that the recovery may not materialize until 2027.

Why Pentair Stock Plunges

Pentair now expects second-quarter sales of approximately $930 million, down 17% from a year ago and well below both Wall Street expectations and the company’s previous guidance.

Adjusted earnings per share are expected to come in around $1.12, missing analyst estimates by a wide margin.

The primary culprit is what management describes as a significant “Pool” channel destocking, which reduced second-quarter sales by approximately $170 million while lowering operating income by roughly $105 million.

What Does “Pool” Mean?

In Pentair’s earnings update, “Pool” refers to the company’s swimming pool equipment business, not a financial pool or investment fund.

Pentair manufactures products used in residential and commercial swimming pools, including:

- Pool pumps

- Filtration systems

- Pool heaters

- Automation and control systems

- Water treatment equipment

- Lighting and cleaning systems

The company’s products are sold primarily through distributors, wholesalers, pool builders, dealers, and retail partners.

Over the past several years, many of those distributors built unusually large inventories following pandemic-era supply shortages. As demand normalized and financing costs rose, distributors began aggressively reducing inventory levels rather than placing new orders with manufacturers such as Pentair.

This process—known as destocking—can significantly reduce manufacturer sales even if demand from homeowners remains relatively stable.

Pentair stock plunges

Pentair Cuts Full-Year Outlook

The weak second quarter prompted management to substantially lower its full-year forecast.

Pentair now expects:

- Revenue between $3.88 billion and $4.01 billion

- Adjusted EPS between $4.60 and $4.80

- GAAP EPS between $3.90 and $4.10

Those figures are significantly below both the company’s previous guidance and Wall Street consensus estimates.

Management estimates that destocking of pool inventory alone will reduce full-year sales by approximately $250 million and operating income by roughly $155 million.

The company also cited elevated interest rates and persistent inflation as additional headwinds affecting demand across the swimming pool market.

Tariff Refunds Offer Partial Offset

One bright spot in the updated guidance is an expected benefit from tariff refunds.

Pentair expects to receive between $35 million and $50 million related to tariffs previously collected under the International Emergency Economic Powers Act (IEEPA).

While those refunds help cushion some of the earnings impact, they are not enough to offset the sharp decline in pool-related sales.

CFO Transition Adds More Uncertainty

Alongside the guidance cut, Pentair announced a leadership change.

Former Chief Financial Officer Bob Fishman will return as interim CFO after Nicholas Brazis departed the company on July 10 to join a private business.

CEO John Stauch emphasized that management believes the inventory correction is temporary.

“We believe these headwinds are temporary and we are taking decisive actions to adapt the business to current demand levels while positioning it to return to normalized performance in 2027.”

Despite the weaker outlook, Pentair repurchased approximately 2 million shares during the second quarter for roughly $150 million, signaling confidence in the company’s longer-term prospects.

Trading Implications

Pentair stock plunges because investors are repricing expectations for earnings growth after management acknowledged that inventory normalization will take longer than previously expected.

For traders, the stock may remain volatile until investors gain confidence that distributor inventories have stabilized and order activity begins recovering.

While Pentair’s Flow and Water Solutions businesses continue performing largely in line with expectations, the swimming pool segment remains the company’s largest source of uncertainty.

Investors should closely monitor inventory commentary from pool equipment distributors, home improvement retailers, and residential construction trends over the coming quarters.

Bottom Line

Pentair stock plunges after the company sharply lowered its 2026 guidance due to a much larger-than-expected inventory correction in its swimming pool equipment business. Although management believes the weakness is temporary and expects conditions to normalize by 2027, investors are likely to remain cautious until distributor inventories stabilize and new orders begin to recover.

With shares now trading at fresh 52-week lows, upcoming earnings on July 28 will be closely watched for additional insight into the timing of that recovery and whether the worst of the inventory reset is finally behind the company.