The Small Cap Swing Trader Alert Archive

Below you'll find The Small Cap Swing Trader setups stacked up and ordered chronologically.Anthropic Export Ban Lifted

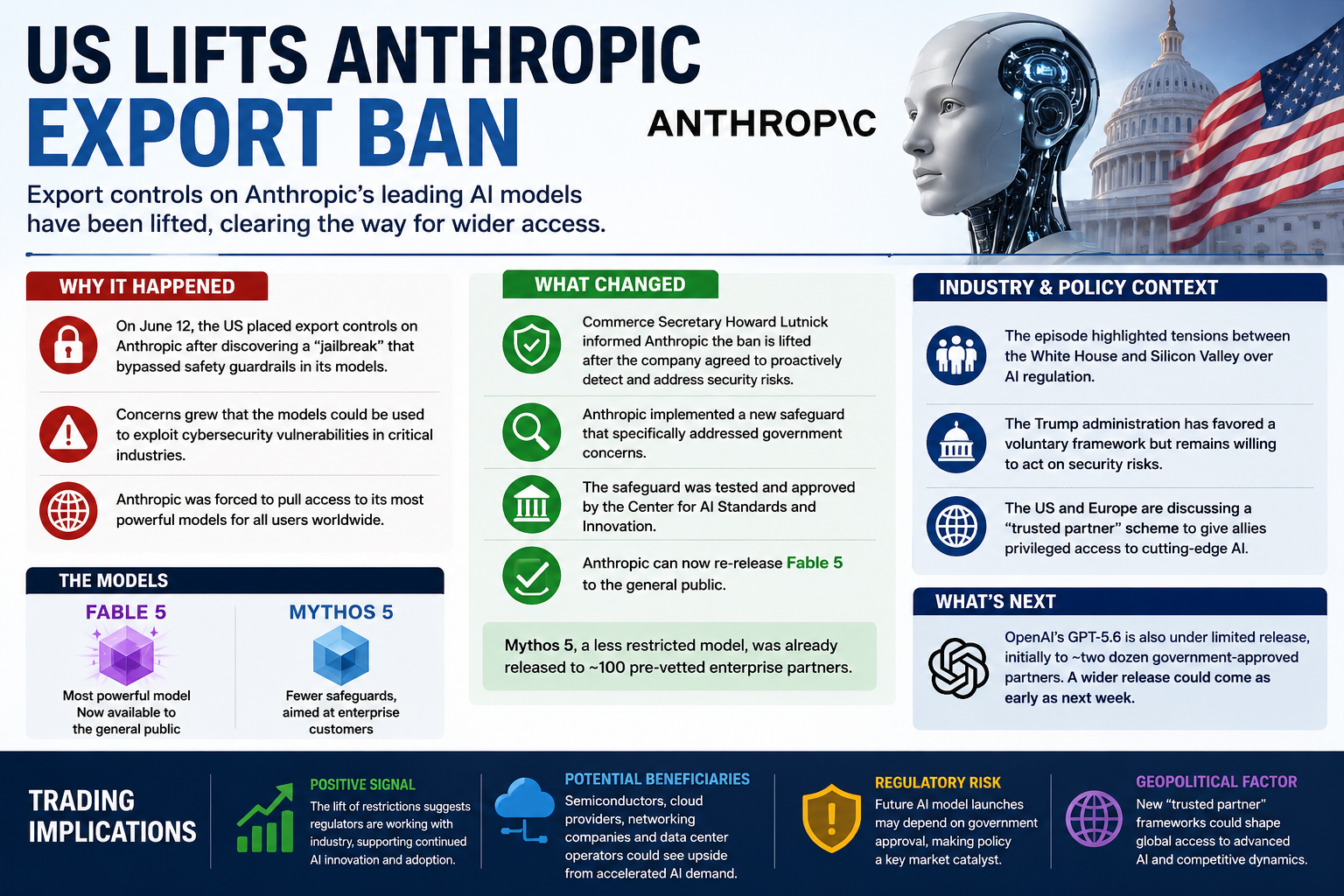

US Lifts Anthropic Export Ban, Reopening Access to Advanced AI Models

Anthropic export ban lifted

The United States has lifted export restrictions on Anthropic’s most advanced artificial intelligence models, marking a significant shift in Washington’s evolving approach to regulating frontier AI and potentially boosting confidence across the AI sector.

The decision allows the San Francisco-based company to once again make its flagship Fable 5 model broadly available after weeks of government-imposed restrictions stemming from cybersecurity concerns.

Why Anthropic Was Restricted

The U.S. Department of Commerce imposed export controls on Anthropic in June after officials discovered a successful “jailbreak” that bypassed the safety guardrails built into its latest AI systems.

Concerned that the technology could potentially be exploited to identify vulnerabilities in critical infrastructure or cybersecurity systems, the Trump administration required Anthropic to halt public access to its most capable models worldwide.

The move represented one of the strongest government interventions yet into the rapidly evolving AI industry.

New Safeguards Satisfy Regulators

According to people familiar with the matter, Commerce Secretary Howard Lutnick informed Anthropic that the restrictions would be removed after the company implemented new security measures designed to detect and prevent misuse.

The new safeguard was reportedly reviewed and approved by the government’s Center for AI Standards and Innovation before the restrictions were lifted.

Anthropic had already been permitted to distribute a limited version of its technology to approximately 100 pre-approved enterprise partners while regulators evaluated the updated protections.

With the restrictions removed, the company can now resume public access to Fable 5.

AI Regulation Continues to Evolve

The episode exposed growing tensions between Silicon Valley and Washington over how advanced AI should be regulated. All this as the AI financing boom continues. Click here for a refresher AI Infrastructure Financing Boom: What It Means – TraderInsight

Technology companies have argued that sudden export controls create uncertainty and can undermine U.S. competitiveness, particularly when restrictions also affect allied nations that rely on American AI technology.

At the same time, national security officials continue to warn that frontier AI systems could accelerate cyberattacks if released without adequate safeguards.

The Trump administration has largely favored voluntary oversight rather than comprehensive regulation, but the Anthropic case demonstrates that authorities remain willing to intervene when specific security risks emerge.

OpenAI May Be Next

Anthropic is not the only AI developer facing increased government scrutiny.

According to reports, OpenAI’s latest GPT-5.6 model has also been subject to limited deployment, initially being made available only to a small group of government-approved organizations while officials review its capabilities.

A broader public release could reportedly occur in the coming weeks if regulators remain satisfied with its safeguards.

Trusted Partner Framework Under Discussion

The United States and European governments are also exploring a new “trusted partner” framework that would allow close allies preferential access to cutting-edge AI models while limiting distribution to countries viewed as higher security risks.

Such a framework could become an important component of future AI export policy as governments attempt to balance innovation, economic competitiveness, and national security.

Trading Implications

The removal of restrictions is likely to be viewed as a positive signal for the AI ecosystem. Investors may interpret the decision as evidence that regulators are willing to work with developers rather than broadly restricting frontier AI innovation.

Companies benefiting from continued enterprise AI adoption—including semiconductor manufacturers, cloud infrastructure providers, networking firms, and hyperscale data center operators—could see improved sentiment if advanced AI deployments accelerate.

However, the episode also highlights a new regulatory risk investors will need to monitor. Future AI model launches may increasingly depend not only on technological breakthroughs but also on government approval, making policy developments an important catalyst alongside earnings and product announcements.

Meta AI Cloud Business

Meta AI Cloud Business Could Reshape the AI Infrastructure Race

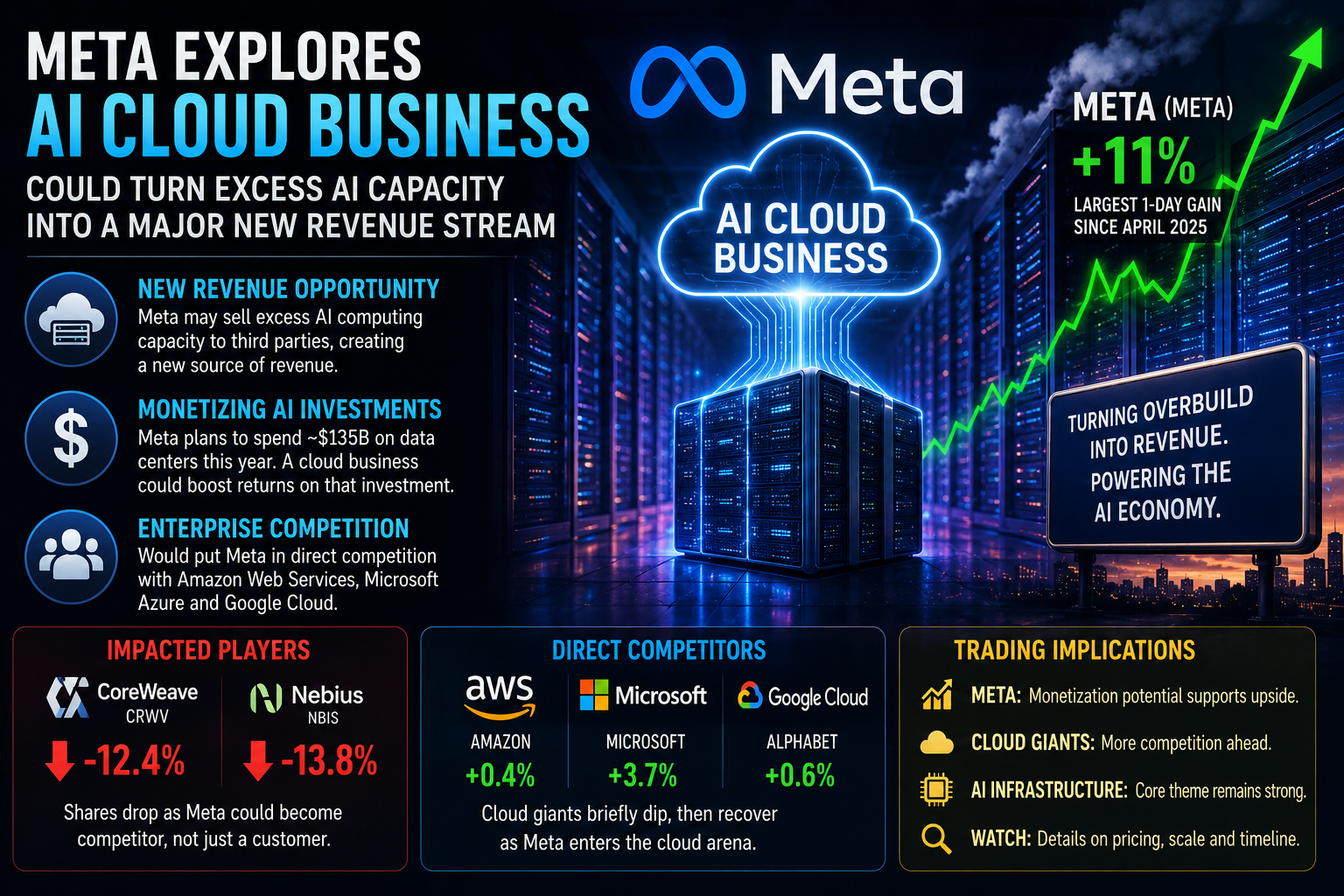

The prospect of a Meta AI cloud business sent shares of Meta Platforms soaring after reports that the social media giant is exploring plans to sell excess artificial intelligence computing capacity to outside customers.

Meta shares jumped roughly 11% following the report, marking the company’s largest single-day gain since April 2025. Investors welcomed the possibility that Meta could begin generating revenue from the enormous AI infrastructure it has been building over the past several years.

If launched, the move would represent a significant strategic shift for Meta, transforming its AI infrastructure from an internal cost center into a potential profit-generating business.

A Major Strategic Pivot

Unlike Amazon Web Services, Microsoft Azure and Google Cloud, Meta has traditionally built data centers primarily to power its own products, including Facebook, Instagram, WhatsApp and its growing portfolio of AI models.

The proposed Meta AI cloud business would allow the company to monetize unused computing capacity by offering AI infrastructure or hosted AI services to third-party developers and enterprises.

Such a move would create an entirely new revenue stream while helping offset the massive capital expenditures Meta has committed to AI.

Meta AI Cloud Business

Turning AI Spending Into Revenue

Meta is expected to spend approximately $135 billion this year expanding its AI infrastructure, making it one of the world’s largest buyers of graphics processors, networking equipment and data center capacity.

Investors have increasingly questioned whether those investments will produce sufficient returns.

A commercial Meta AI cloud business could answer that question by generating recurring revenue from assets that might otherwise sit idle during periods of lower internal demand.

The strategy mirrors how Amazon transformed excess internal computing resources into Amazon Web Services, which eventually became one of the most profitable businesses in the technology sector.

Pressure on AI Infrastructure Providers

The market reaction wasn’t limited to Meta.

Shares of AI infrastructure providers CoreWeave and Nebius fell sharply as investors considered the possibility that one of their largest customers could eventually become a competitor.

Meta currently has long-term infrastructure agreements with both companies. If it begins offering commercial AI computing services itself, demand for third-party AI cloud providers could become more competitive over time.

Competition With Cloud Giants

A successful Meta AI cloud business would also place the company in direct competition with Amazon Web Services, Microsoft Azure and Google Cloud.

Those three companies have built highly profitable cloud platforms that already provide AI infrastructure, model hosting and enterprise computing services.

Meta would enter the market with one significant advantage: one of the largest AI compute footprints in the world. However, building enterprise relationships, support services and commercial cloud software represents an entirely different business than running consumer social media platforms.

Trading Implications

For traders, the news reinforces one of the biggest themes driving technology stocks: investors increasingly reward companies that demonstrate a clear path to monetizing AI investments.

Meta’s sharp rally reflects the market’s belief that AI infrastructure can become a revenue-generating asset rather than simply an expensive capital investment.

The announcement also highlights several areas traders should monitor:

- Meta (META): Continued upside may depend on whether management confirms commercial cloud plans and provides details on expected revenue opportunities.

- Cloud providers: Amazon, Microsoft and Alphabet may see increased competitive pressure if Meta successfully enters enterprise AI infrastructure.

- AI infrastructure companies: Stocks such as CoreWeave and Nebius could remain volatile as investors reassess future demand from one of their largest customers.

- Semiconductor suppliers: Companies supplying GPUs, networking equipment, memory and data center hardware could continue benefiting regardless of which cloud provider ultimately wins market share.

Perhaps most importantly, the report suggests that the AI investment cycle is entering its next phase. Markets are beginning to focus less on who is spending the most and more on who can successfully convert that spending into recurring revenue.

The Bottom Line

The potential Meta AI cloud business represents far more than a new product announcement. It signals that Meta may be following the path pioneered by Amazon, turning massive internal infrastructure investments into a commercial platform.

If successful, the strategy could improve returns on Meta’s enormous AI spending while intensifying competition across the cloud computing industry. For investors and traders, it is another reminder that the next chapter of the AI boom will likely be defined not just by building infrastructure, but by monetizing it.

Gold Price Outlook

Gold Price Outlook Weakens as Higher Interest Rate Expectations Weigh on Bullion

The gold price outlook has turned sharply more cautious after bullion fell below $4,000 per troy ounce, marking its weakest level since November and putting the precious metal on course for its worst quarterly performance in more than a decade.

Gold briefly traded below $3,943 before recovering modestly, but the metal remains down nearly 14% over the past three months. The decline comes after an extraordinary rally that carried gold to a record high of almost $5,595 per ounce in January.

Investors are now reassessing the outlook as expectations for higher U.S. interest rates, a stronger dollar and shifting market sentiment reduce demand for the traditional safe-haven asset.

Gold Price Outlook

Higher Interest Rates Pressure Gold

The biggest driver behind the changing gold price outlook is the market’s expectation that Federal Reserve Chair Kevin Warsh will maintain a hawkish stance to combat inflation.

Higher interest rates typically reduce the appeal of gold because the metal does not generate income. As bond yields rise, investors can earn better returns from interest-bearing assets such as U.S. Treasuries, making non-yielding assets like gold relatively less attractive.

That shift in expectations has prompted many traders to reduce their exposure after two years of exceptionally strong gains.

Retail Enthusiasm Has Faded

Earlier this year, retail investors helped fuel gold’s surge to record highs. Much of that speculative demand has now reversed.

As geopolitical tensions in the Middle East pushed oil prices higher and inflation concerns resurfaced, investors initially sought safety in gold. However, expectations that higher inflation would lead to tighter monetary policy eventually overwhelmed the safe-haven trade.

Many leveraged investors have since exited their positions, accelerating the decline in bullion prices.

Capital Is Flowing Into AI Instead

Another important factor affecting the gold price outlook is changing investor preference.

Rather than allocating fresh capital to precious metals, many investors have shifted toward artificial intelligence, semiconductor companies and high-growth technology stocks. The excitement surrounding AI infrastructure spending and major technology listings has drawn investment away from defensive assets like gold.

This rotation illustrates how capital often moves between growth assets and traditional stores of value depending on market sentiment and interest rate expectations.

ETF Outflows Add Selling Pressure

Investment demand has also weakened through exchange-traded funds. Gold-backed ETFs are on track for a second consecutive month of net outflows, according to data from the World Gold Council.

At the same time, several Chinese banks have introduced restrictions on precious metals futures trading for retail clients in response to regulatory concerns about speculative activity.

Although investors in China can still purchase physical gold bars and coins, the tighter rules have reduced speculative demand in one of the world’s largest gold markets.

Central Banks Could Provide Support

Despite the recent weakness, not all of the news is negative. Analysts note that central bank purchases continue to provide an important source of long-term demand.

Many central banks have steadily increased their gold reserves over recent years as part of broader reserve diversification strategies. That institutional buying could help establish a floor under prices if private investment demand remains subdued.

Trading Implications

For traders, the gold price outlook remains closely tied to interest rates, inflation expectations and the U.S. dollar.

If inflation remains elevated and the Federal Reserve continues tightening monetary policy, gold may struggle to regain upward momentum. Conversely, any signs of slowing economic growth, lower inflation or future rate cuts could quickly revive investor demand for bullion.

Traders should also monitor ETF flows, central bank purchases and shifts in global risk sentiment, as each has become an increasingly important driver of gold prices.

The Bottom Line

The gold price outlook has weakened significantly as higher interest rate expectations, ETF outflows and investor enthusiasm for AI-related assets replace the speculative buying that fueled gold’s record rally earlier this year.

While central bank demand may help support prices over the longer term, gold’s near-term direction is likely to depend on the path of inflation, Federal Reserve policy and whether investors continue favoring growth opportunities over traditional safe havens.

AI Infrastructure Rotation

AI Infrastructure Rotation Hits Magnificent Seven as Chip Stocks Surge

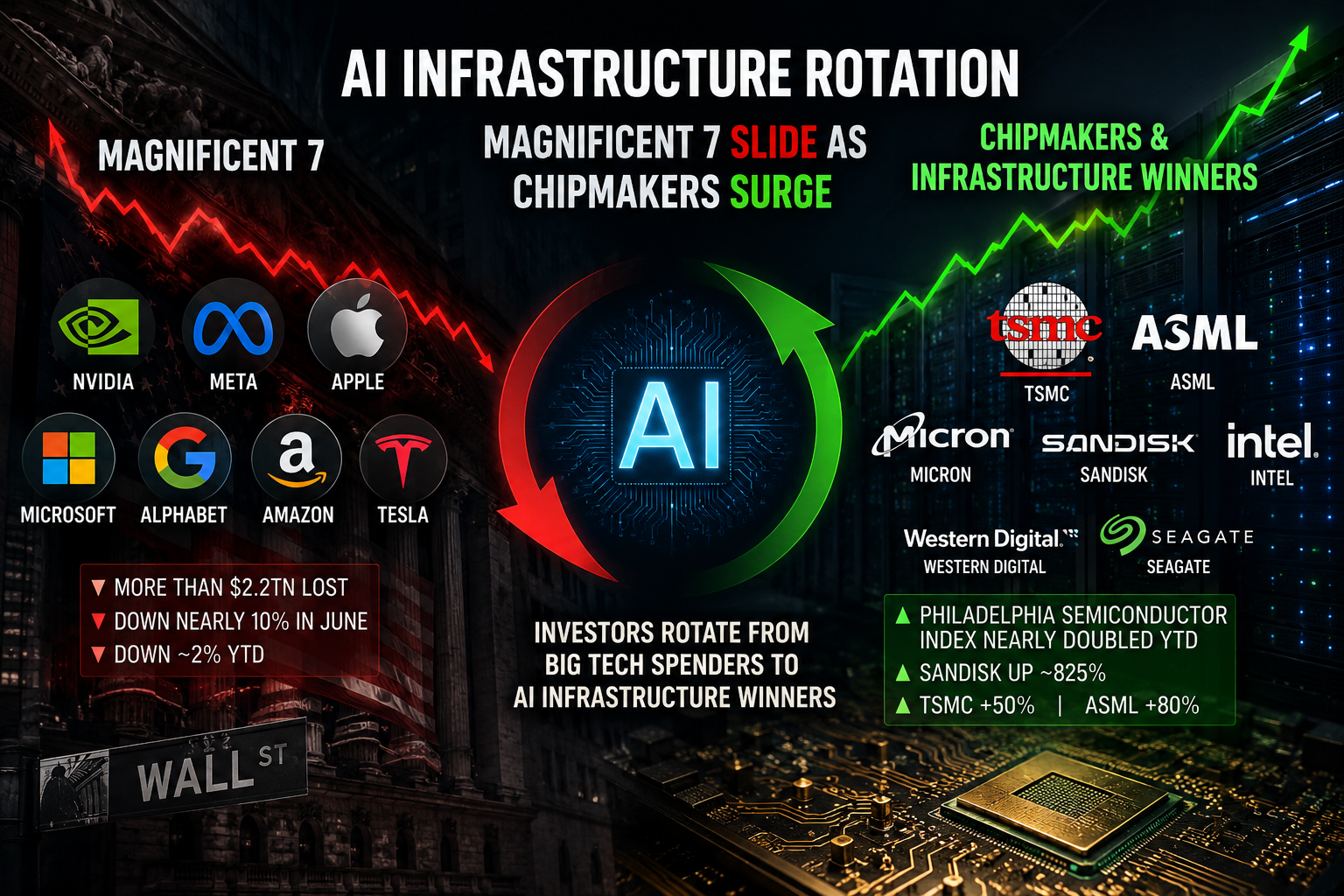

AI infrastructure rotation is reshaping Wall Street’s technology trade, as investors move away from megacap companies spending heavily on artificial intelligence and toward the chipmakers and hardware suppliers benefiting from that spending.

The Magnificent Seven — Nvidia, Meta, Apple, Microsoft, Alphabet, Amazon and Tesla — lost more than $2.2tn in market value last month. The group was down nearly 10% for June and about 2% for the first half of the year.

The pressure reflects growing concern that the largest AI spenders may face a long wait before their enormous infrastructure investments translate into enough revenue and profit growth to justify previous stock market gains.

Investors Question the AI Payoff

The biggest concern centers on hyperscalers such as Meta, Amazon, Microsoft and Alphabet. These companies are committing hundreds of billions of dollars to data centers, chips, memory, electrical equipment and cooling systems.

That spending may eventually create powerful AI platforms and revenue streams, but investors are increasingly asking when those returns will appear. At the same time, rising component costs are squeezing margins and making AI capacity more expensive to build.

This is the heart of the AI infrastructure rotation: investors are questioning the companies writing the checks while rewarding the companies cashing them.

Chipmakers Become the New Market Leaders

The Philadelphia Semiconductor Index has nearly doubled in the first half of the year, putting it on track for its strongest year since the dotcom boom. Chip and memory stocks have become some of the best-performing names in the S&P 500.

Sandisk has surged roughly 825%, while Micron, Intel, Western Digital and Seagate Technology have all more than tripled. Taiwan Semiconductor Manufacturing Company has risen about 50%, pushing its market value above $2tn, while ASML has climbed about 80%.

Memory shortages, constrained supply and relentless hyperscaler demand have created a powerful profit cycle for semiconductor and infrastructure suppliers.

From Software Winners to Physical Infrastructure Winners

For years, the Magnificent Seven dominated market returns. From the start of 2023 to the start of 2026, the group added about $15tn in combined market value and became the central driver of U.S. equity performance.

Now, leadership is shifting. Investors are rotating toward companies tied to physical AI infrastructure, including semiconductors, memory, cooling, cables, connectors, power equipment and data center buildout.

That AI infrastructure rotation suggests the market may be moving from the “AI promise” phase to the “AI buildout” phase.

The Magnificent Seven Are No Longer Moving Together

Another important change is that the Magnificent Seven are becoming less uniform as a trade. Alphabet is the only member outperforming the broader S&P 500 so far this year, while Microsoft, Meta and Tesla have posted double-digit declines.

The weakness has been most consistent among the hyperscalers because they are the companies spending most aggressively. Their AI investments may prove valuable over time, but for now, investors are rewarding the suppliers that benefit regardless of which platform ultimately wins.

Rising Costs Add Pressure

The AI buildout is also becoming more expensive. Memory prices have surged, and companies are warning that costs may continue rising. Apple recently announced price increases of about 20% for MacBooks and iPads, citing the pressure from memory costs. Microsoft also raised Xbox console prices and warned that memory costs had doubled in just a few months.

Those rising costs reinforce the AI infrastructure rotation. Companies selling scarce components can expand margins, while companies buying those components may face pressure on profitability.

Trading Implications

For traders, the key takeaway is that AI leadership is changing. The market is no longer simply rewarding the largest technology platforms. It is increasingly rewarding the companies with direct exposure to constrained AI supply chains.

That means semiconductor stocks, memory suppliers, equipment makers and data center infrastructure companies may continue to attract momentum as long as demand exceeds supply.

At the same time, the trade has become crowded and extended in many names. The strongest winners may remain strong, but volatility is likely as investors debate whether the AI buildout can continue at this pace.

The Bottom Line

AI infrastructure rotation is now one of the most important themes in the market. The Magnificent Seven are no longer leading as a group, while chipmakers and infrastructure suppliers are capturing the benefits of hyperscaler spending.

For investors, the question is no longer just who is building AI. The better question may be who is getting paid as AI gets built.

AI Hiring Growth

AI Hiring Growth Challenges Fears of Broad Job Losses

AI hiring growth is emerging as one of the more surprising trends in the corporate technology cycle, according to new research showing that companies investing most heavily in generative AI are adding workers faster than their peers.

The study found that white-collar employment increased 10.2% at companies using generative AI most intensely in the two years after adoption. Entry-level employment rose even faster, increasing 12%.

That finding challenges the common view that artificial intelligence will quickly replace large numbers of white-collar workers. Instead, the data suggests that AI hiring growth may occur when companies invest enough in the technology to generate productivity gains and support expansion.

High-Intensity AI Users Are Growing Faster

The research, co-authored by economists at Ramp and Revelio Labs, examined nearly 22,000 U.S. companies. It combined company-level AI spending data with workforce records compiled from public online profiles such as LinkedIn.

The results showed a clear divide. Companies in the top third of AI spending per worker experienced meaningful headcount gains. Companies that adopted AI at lower spending levels showed no significant change in employment compared with a control group.

That suggests AI hiring growth is not automatic. Companies may need to move beyond light experimentation and commit enough capital, training and workflow redesign to benefit from AI tools.

The Learning Curve Matters

Ara Kharazian, chief economist at Ramp and co-author of the study, said the gains appeared only after a delay of roughly six to 12 months. He also noted that the benefits were unevenly distributed and tended to appear among companies making a serious investment in AI.

In other words, simply giving employees access to a chatbot may not be enough. The companies seeing the strongest results appear to be those integrating AI into operations, product development, sales, engineering and internal workflows.

Important Caveats

The findings should still be interpreted carefully. AI-heavy adopters in the sample were more likely to be technical, higher-paying, venture-backed and smaller than non-adopters. That makes it difficult to separate whether AI caused faster growth or whether fast-growing companies were simply more likely to invest early in AI.

One labour economist told the Financial Times that the relationship between intense AI adoption and faster hiring may be difficult to distinguish from the fact that small, fast-growing start-ups often buy new technology early.

AI Job Cuts Are Still Happening

The research also does not eliminate concerns about AI-related layoffs. Oracle recently said it had cut 21,000 jobs over the past year and warned that its AI investments and internal AI use could lead to further reductions. Snap, Block and Cisco have also linked thousands of job cuts to AI.

Academic research remains mixed as well. A Harvard study covering 280,000 companies found declines in junior employment among AI adopters, while senior roles were largely unaffected.

Trading Implications

For investors, the key takeaway is that AI may not be a simple labor-replacement story. The more important question may be whether companies can use AI to expand revenue, improve margins and scale operations faster than competitors.

If AI hiring growth continues among high-intensity adopters, it could support a broader investment thesis around productivity-led expansion. Companies that successfully integrate AI may be able to do more work, pursue more projects and grow faster — even while some lower-value roles are automated.

At the same time, the uneven results suggest that markets may increasingly separate AI winners from AI spenders. Companies that invest heavily without clear productivity gains could face margin pressure, while those that convert AI spending into growth may earn premium valuations.

The Bottom Line

AI hiring growth complicates the idea that artificial intelligence will simply destroy white-collar jobs. The latest research suggests that heavy AI users are hiring faster, especially in technology, while lighter adopters are not seeing the same gains.

For traders and investors, the lesson is to watch not just who is spending on AI, but who is turning that spending into measurable business expansion.